What financial milestones should I hit before I can retire comfortably? It is a question worth sitting with seriously. Picture this: a 50-year-old director at a well-known Malaysian corporation, a solid EPF balance sitting comfortably above RM300,000, a unit trust portfolio ticking along, no major financial complaints. Yet quietly, almost privately, she is unsure whether any of it truly adds up. She has savings. But is she genuinely retirement-ready? These are not the same thing, and confusing the two is a blind spot many high-earning professionals in Malaysia share.

Retirement readiness is not a single number you hit and move on from. It is a checklist of interconnected milestones covering your savings depth, debt position, passive income, insurance coverage, and estate basics. Miss one, and the whole plan can unravel faster than you expect. This article walks through five concrete milestone areas with specific Malaysian targets and age-based benchmarks so you can assess exactly where you stand today.

Table of Contents

The age-income savings multiple: your first readiness signal

The most practical starting point for any honest retirement readiness assessment is comparing your total retirement savings to a multiple of your current annual gross income. The benchmarks that most advisers broadly converge on are: 1× your income by age 30, 3× by 40, 5, 6× by 50, 7× by 55, and 10× by your mid-to-late 60s. These multiples align closely with frameworks published by major global financial institutions, and Malaysian financial commentators have adopted broadly similar targets. If you earn RM120,000 a year and you are 45, you should be tracking toward RM480,000, RM600,000 in total retirement savings, not just your EPF balance alone. For a practical read on age-based saving benchmarks, see guidance on how much you should have saved by age.

What counts toward this multiple matters enormously. Your figure must include EPF, voluntary contributions, unit trust portfolios, REITs, fixed deposits, Private Retirement Scheme (PRS) accounts, and any other investable assets genuinely earmarked for retirement. Professionals who count only their EPF balance routinely underestimate how far behind they are, because EPF is one component of a complete retirement picture, not the whole answer.

What EPF’s 2026 benchmarks actually tell you

EPF’s updated Retirement Income Adequacy (RIA) framework, effective January 2026, sets a Basic Savings threshold of RM390,000 by age 60, yielding a Year 1 monthly payout of approximately RM1,625. The Adequate tier requires RM650,000 by age 60, generating roughly RM2,708 per month. These figures are revealing: Malaysian financial planners consistently associate a genuinely comfortable urban retirement with RM5,000, RM6,500 per month, meaning EPF’s Adequate tier still leaves a significant shortfall. EPF is a foundation, not a complete retirement income strategy. Recent commentary also notes that many Malaysians are choosing to top up and save longer to bridge gaps left by statutory provisions (EPF says more Malaysians saving for longer).

Calculating your personal retirement corpus in ringgit

Once you know your savings multiple position, the next step is working backwards from your desired retirement lifestyle to a specific ringgit target. This is where most self-assessments break down entirely. People skip the arithmetic, assume they are roughly on track, and discover the gap far too late to close it comfortably.

The 70, 80% income replacement ratio explained

Malaysian financial planners broadly recommend targeting 70, 80% of your pre-retirement monthly income as your retirement income goal. If your household currently lives on RM10,000 a month, you are targeting RM7,000, RM8,000 per month in retirement income. Some expenses do fall away, mortgage payments and children’s education costs typically reduce, but healthcare expenses generally rise with age, offsetting much of that saving. Do not assume your retirement will be significantly cheaper than your working life; for most professionals, the difference is smaller than expected.

A simple formula to reverse-engineer your RM target

For Malaysian retirement planning, a conservative working assumption is a nominal investment return of 5, 6% per annum and an inflation rate of 3%, giving a real return of roughly 2, 3%. Using a conservative 2% real return and a 25-year retirement horizon from age 60 to 85, a target income of RM6,000 per month (RM72,000 per year) requires a corpus of approximately RM1.4 million, RM1.8 million. The lower end reflects a 2% real-return annuity over 25 years; a higher figure accounts for elevated Kuala Lumpur living costs and a more cautious inflation buffer. If you are based in Kuala Lumpur, planners often cite RM2 million or above as a more realistic floor. Calculate your specific number before you decide you are on track, a general impression of “I have savings” is not a retirement plan.

A retirement readiness calculator can help you stress-test these projections against your own income, age, and target lifestyle, it is worth running the numbers before drawing any conclusions about where you stand.

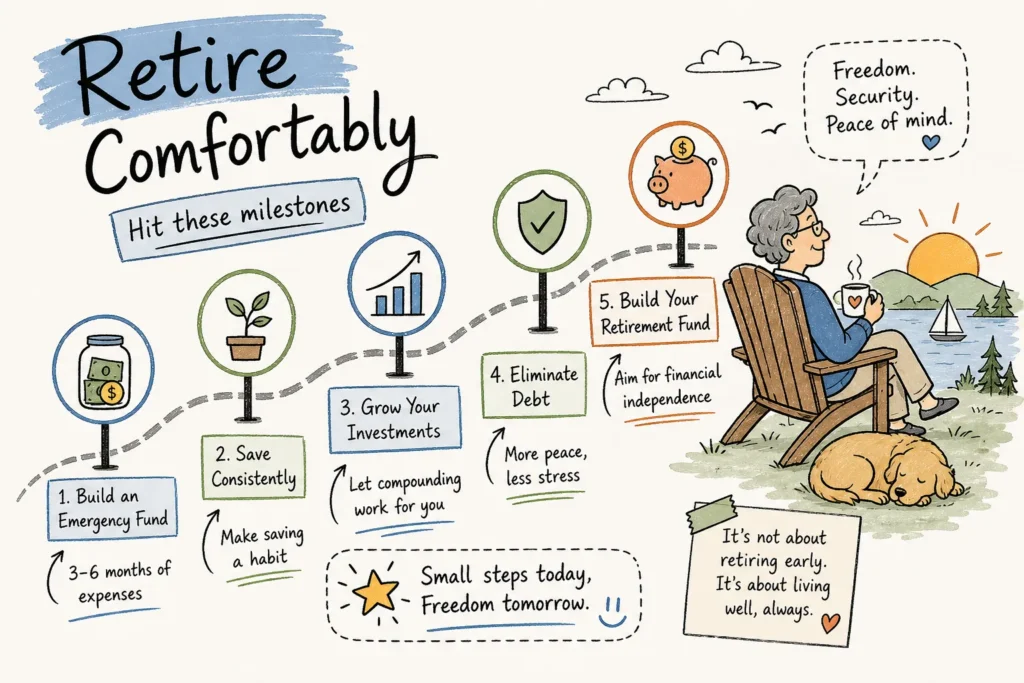

Checklist: financial milestones to hit before you retire comfortably

Before examining each milestone in detail, it helps to see them together. The five areas that determine whether you can retire comfortably are: your savings multiple relative to income, a personalised corpus target in ringgit, a debt-free and adequately buffered cashflow position, comprehensive medical and critical illness coverage, and a passive income structure backed by basic estate planning. The sections below walk through each one in turn.

Debt freedom and emergency reserves before you stop working

Entering retirement with outstanding debt is one of the most costly planning oversights among Malaysian professionals. Every ringgit directed toward loan repayments in retirement is a ringgit that cannot fund your living expenses, and there is no monthly salary to replace what is lost. This is not a minor inconvenience; it is a structural problem that compounds through every retirement year.

Why zero debt before retirement is a non-negotiable milestone

The standard benchmark is 100% debt-free at retirement: no outstanding mortgage, no car loan, no personal financing. A household carrying RM2,000 per month in loan repayments into retirement effectively needs a corpus that is RM480,000, RM600,000 larger than it would otherwise require, based on a 20-to-25-year repayment horizon, just to service that one obligation. Clearing your highest-interest debt first, then accelerating mortgage paydown from your 50s onward, should be a deliberate and scheduled strategy. Leaving this as an afterthought for your final working year carries a real and avoidable cost.

Sizing your pre-retirement emergency buffer correctly

Beyond debt, you need a liquid emergency fund of 3, 6 months of essential living expenses sitting in an immediately accessible account, completely separate from your investment portfolio. For a household spending RM5,000 per month on essentials, that means RM15,000, RM30,000 in reserve. Those with variable or freelance income should hold closer to 12 months. This buffer exists to protect your portfolio from forced early withdrawals during market downturns, one of the primary drivers of sequence-of-return risk in the early retirement years, the period when your portfolio is most vulnerable to permanent capital loss.

Medical and critical illness coverage: the milestone most professionals overlook

A retirement corpus that looks sufficient on paper can be wiped out by a single uninsured health event. For Malaysian retirees, an unplanned medical episode is among the most common reasons savings are exhausted ahead of schedule, and it happens to professionals with otherwise well-structured financial plans.

What adequate medical coverage looks like heading into retirement

Given current private hospital costs in Malaysia and a medical inflation rate running at approximately 12% annually (based on insurer and industry data), planners increasingly recommend a medical card with an annual limit of at least RM200,000 per admission as a minimum floor for those in their 40s and 50s, with many advocating RM1 million or above for comprehensive protection at top-tier private hospitals. A comprehensive critical illness policy, many currently available plans cover 36 or more major conditions, is equally important as a separate layer of financial protection. The time to secure comprehensive coverage is before health conditions emerge, when premiums are still manageable and insurers will still underwrite you.

How to assess whether your current coverage has gaps

Review your medical card’s annual limit, room and board coverage, and whether it extends to outpatient specialist consultations. Many professionals purchased their first medical plan in their 30s and have never reviewed it since, leaving them with annual limits that no longer reflect current hospital fees. A coverage gap of even RM50,000 per health event can put pressure on your investments at the worst possible time, permanently damaging your retirement income trajectory. An insurance review is not an optional exercise; it is a critical part of your retirement checklist.

Passive income and estate planning: the final two milestones

Financial readiness for retirement is not just about accumulating a large enough corpus. It is about structuring that corpus to generate reliable, sustainable income without requiring you to actively manage it daily, and ensuring that income flows correctly to your dependants if something happens to you.

The passive income coverage ratio as a retirement signal

A useful milestone is whether your passive income sources, EPF drawdowns, dividend-paying equities, REIT distributions, rental income, or fixed deposit interest, can cover at least 80, 100% of your monthly retirement expenses without drawing down your principal. Malaysian retirees increasingly draw on dividend stocks from blue-chip institutions, REITs offering mandated 90% profit distributions, and rental property to supplement EPF withdrawals. If your passive income currently covers only 40, 50% of your projected retirement expenses, you are heavily dependent on capital depletion, which accelerates the risk of outliving your savings across a 25, 30 year retirement horizon.

The estate planning essentials every Malaysian pre-retiree needs in place

Estate planning is the most deferred milestone on this checklist, and the consequences of ignoring it are severe. At a minimum, every Malaysian pre-retiree should have a valid civil will (or wasiat for Muslims), an updated nomination on all EPF accounts, and an updated nomination on all insurance policies. For more complex estates, a hibah arrangement or trust structure may help ensure assets transfer efficiently outside the probate process. Without these documents in order, assets can be frozen for years, leaving dependants without access to funds during precisely the period they need them most. For straightforward estates, the core documents, will, EPF nomination, insurance nomination, can typically be put in place within a matter of weeks with the right professional guidance.

Not sure you have genuinely checked every box?

Reading a checklist and knowing whether you have truly met each milestone are two entirely different things. Many financially literate professionals can tick these items in theory but have never run the actual numbers against a personalised retirement timeline, stress-tested their portfolio against a 30-year horizon with realistic inflation assumptions, or had their insurance coverage independently reviewed by someone with no financial interest in what you purchase next.

The challenge with self-assessment is that you are evaluating your own assumptions. You may be using an inflation rate that is too optimistic, overestimating EPF growth, holding insurance policies that no longer match your income level, or missing a gap in your estate documentation that will create significant problems later.

A fee-based CFP operating on a flat-fee model, with no commissions and no products to sell, will run your numbers independently, identify gaps across all five milestone areas, and give you a clear picture of where you actually stand. A structured retirement readiness review, such as that offered by CF Lieu, Wealth Advisor, is designed specifically for mid-career professionals and pre-retirees who want honest, unbiased answers. The review covers savings adequacy against your income multiple, a personalised corpus projection in ringgit, cashflow stress-testing, insurance gap analysis, and estate planning basics, all within a flat-fee engagement with no sales agenda attached to the findings.

What financial milestones should I hit before I can retire comfortably, where do you actually stand?

The financial milestones that determine whether you can retire comfortably are not complicated, but they require honest, numbers-based assessment across five dimensions: your savings multiple relative to income, your personalised retirement corpus in ringgit, a debt-free and adequately buffered cashflow position, comprehensive medical and critical illness coverage, and a passive income structure backed by basic estate planning. Most professionals are strong in one or two of these areas and quietly underprepared in others.

Knowing which category you fall into is the starting point. Your savings multiple shows how your accumulation phase is tracking. The corpus calculation gives you the specific ringgit target you are working toward. The debt and buffer assessment reveals whether your cashflow structure can sustain retirement without early portfolio liquidation. The insurance review tells you whether a health event could derail everything. And the estate plan determines whether your family will actually benefit from what you have spent decades building. None of these milestones work in isolation, all five must be in order before you can genuinely call yourself retirement-ready.

If you have read through these milestones and still feel uncertain about where your finances truly stand, that uncertainty is worth acting on now, while the options remain open and the time horizon still allows for meaningful course correction. For actionable next steps and targeted checklists on improving your retirement readiness, see 18 Quick Tips to improve retirement planning in Malaysia.

FAQs: Financial Milestones to Retire Comfortably

What savings multiple should I aim for at different ages to be retirement-ready?

Use age-based income multiples as a quick readiness signal: about 1× your income by 30, 3× by 40, 5–6× by 50, 7× by 55 and roughly 10× by your mid-to-late 60s. These benchmarks reflect broad adviser consensus referenced in the article and help you see whether total retirement savings are tracking to your income level.

Can I rely on EPF alone to fund a comfortable retirement?

No — EPF is a foundation, not the complete solution. EPF’s RIA framework (effective January 2026) sets Basic savings at RM390,000 (about RM1,625/month Year 1) and Adequate at RM650,000 (about RM2,708/month), but many planners say a comfortable urban retirement typically needs RM5,000–RM6,500/month, so most people will face a shortfall without additional savings.

What assets should I include when calculating my retirement savings multiple?

Include all investable assets genuinely earmarked for retirement: EPF, voluntary contributions, unit trust portfolios, REITs, fixed deposits, Private Retirement Scheme (PRS) accounts and any other similar holdings. Counting only EPF commonly causes people to underestimate how far behind they are.

How do I convert my desired retirement lifestyle into a ringgit corpus target?

Start with a target retirement income equal to about 70–80% of your pre-retirement monthly income (for example, RM10,000 now implies RM7,000–RM8,000 in retirement). Then work backwards using expected income sources, expected withdrawals and longevity assumptions, remembering that some expenses (mortgage, children) may fall but healthcare often rises, so do the arithmetic rather than assuming you’re on track

What other milestone areas besides savings should I check before retiring?

Assess five interconnected milestone areas: depth of savings, debt position, passive income streams, insurance coverage and basic estate planning. Missing any one of these can undermine retirement readiness even if your savings look adequate.

If I’m 50 with about RM300,000 in EPF and some unit trusts, am I retirement-ready?

You need to total all retirement assets and compare them to the age-income multiple target for 50 (around 5–6× your current annual income). Also evaluate debt, passive income, insurance and estate basics; having RM300,000 in EPF plus unit trusts may still leave you short of the realistic lifestyle income you want in retirement.

How can Malaysians bridge the gap between EPF payouts and a comfortable retirement income?

Common approaches are topping up savings, saving for longer, and using other retirement vehicles such as PRS, unit trusts, REITs and fixed deposits to build investable assets for retirement. The article notes many Malaysians are choosing to top up and extend their working years to close the gap left by statutory provisions.