Picture this: a 45-year-old manager based in Petaling Jaya, earning well, contributing faithfully to EPF every month, and sitting on a balance she has never really interrogated. She knows the number looks respectable. What she does not know is whether it is actually enough, enough for how long, enough for what kind of life, enough to avoid going back to work at 70.

That uncertainty is precisely what this retirement planning milestones by age guide is designed to resolve. Rather than leaving you to guess, it gives you a concrete benchmark at every decade of your working life: a clear checkpoint that tells you whether you are on track, ahead, or quietly falling behind. The savings multiples referenced throughout are drawn from Fidelity’s widely cited retirement savings framework, specifically their age-based salary multiples, adapted here to the Malaysian context with EPF contribution structures, PRS tax rules, and local life expectancy data in mind. Where local EPF cohort averages or Malaysian financial planning conventions differ meaningfully from the global framework, those distinctions are noted explicitly.

One important caveat upfront: benchmarks are a starting point, not a verdict. They do not account for your specific lifestyle, whether you plan to retire at 55 or 62, how many dependants you support, or what your actual spending looks like in retirement. A personalised stress-test from a fee-only financial planner can tell you whether these numbers hold for your specific situation. But you need the benchmarks first, and this retirement timeline checklist gives you all of them.

Table of Contents

Why Malaysians Need Age-Pegged Retirement Milestones

The Retirement Runway Is Longer Than Most People Expect

Malaysia’s official retirement age for the private sector is 60, but average life expectancy sits at approximately 75 to 77 years overall, with women typically living to 77 to 78 years. That means the average retiree needs to fund 15 to 20 years of living expenses from their savings, EPF balance, and investment income alone. Women face a structurally greater longevity risk: a longer retirement runway on a savings pot that is often smaller due to career interruptions. The common assumption that EPF will simply “cover it” underestimates this reality significantly.

EPF data reinforces the concern. According to the EPF 2024 Annual Report, the average savings for active members aged 50 to 54 stands at RM237,426, well below EPF’s own basic savings benchmark of RM290,000, which became effective in 2026. Only about 18% of EPF members had met the basic savings benchmark at retirement age as of the EPF’s most recently published data, meaning roughly 82% fall short. These are not outliers or the financially reckless; they are ordinary, working Malaysians who simply did not have a clear retirement savings target to aim for.

The 70, 80% Income Replacement Target

Malaysian financial planners generally recommend targeting 70 to 80% of your pre-retirement income as your monthly retirement income. For a professional earning RM10,000 per month, that translates to RM7,000 to RM8,000 per month needed in retirement. A rough EPF balance figure tells you very little on its own without running it through this income-conversion lens. You need both a savings multiple and a monthly income projection to get an honest picture of your readiness.

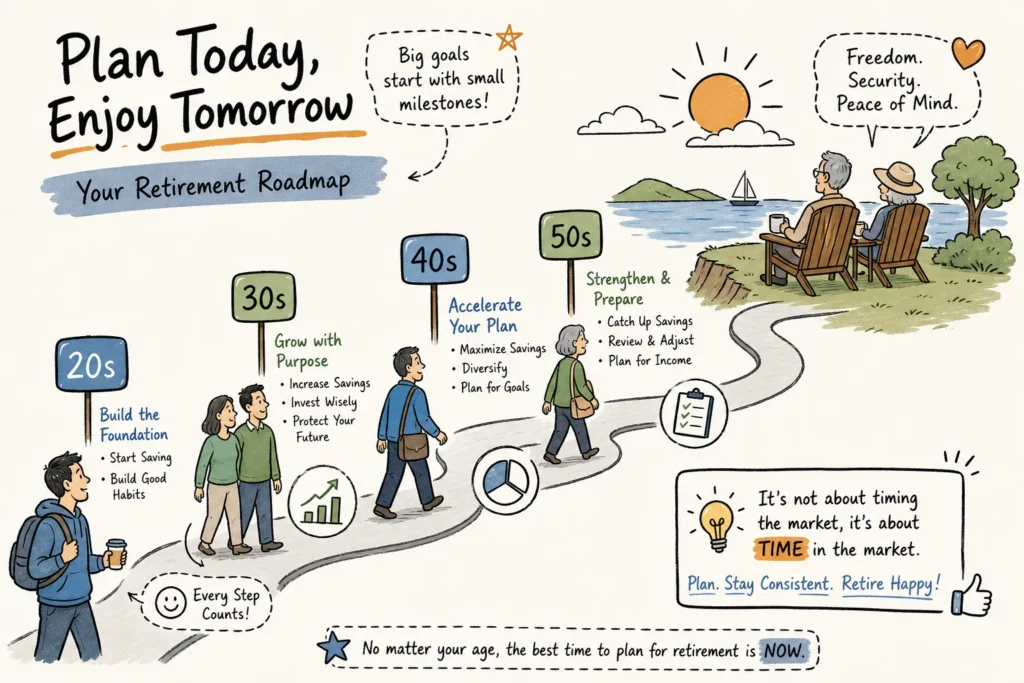

Retirement Planning Milestones by Age: Your 30s

The 1x, 2x Salary Benchmark in Ringgit Terms

The savings multiple framework sets a clear first target: 1x your annual salary saved by age 30, rising to 2x by age 35. For a 32-year-old HR executive in Kuala Lumpur earning RM7,000 per month (RM84,000 per year), that means RM84,000 to RM168,000 across EPF, unit trusts, and other retirement savings combined. The metric covers all retirement savings, not EPF alone. Some professionals in their early 30s may find their EPF balance tracks close to 1x if they entered the workforce at 22 or 23 and have not made significant withdrawals, though this depends on starting salary, salary growth, and withdrawal history.

The compounding mathematics of this decade are irreplaceable. Every ringgit saved at 30 has a 25-to-30-year runway to grow before retirement. Missing this window does not simply delay progress; it forces you to save two to three times as much later to achieve the same outcome. Evidence and common planning wisdom consistently show that starting early materially increases the likelihood of a comfortable retirement, even for moderate earners.

EPF, PRS, and Your First Term Life Cover

The standard EPF contribution structure, 11% from the employee, with the employer contributing 13% for salaries at or below RM5,000 and 12% for salaries above RM5,000, is a solid floor, but rarely sufficient on its own for a comfortable 20-year retirement. PRS is the natural complement: contributions of up to RM3,000 per year qualify for standalone tax relief until assessment year 2030, entirely separate from the RM4,000 EPF relief. Starting PRS contributions in your 30s locks in the tax benefit for decades and builds a second accumulation pool outside EPF.

Term life insurance is the milestone most commonly skipped in this decade. Anyone with dependants, a mortgage, or a spouse who relies on their income should hold coverage of 10 to 12 times their annual income, a widely used rule of thumb among Malaysian financial planners. A RM84,000-per-year earner needs RM840,000 to RM1,008,000 in term coverage. This is not a wealth-building instrument; it is a financial foundation. Without it, a single unforeseen event can permanently derail every other milestone on this list.

Your 40s: The Power Decade for Wealth Accumulation

Hitting the 3x, 4x Salary Target and What Corporate Professionals Commonly Miss

By age 40, the savings benchmark rises to 3x your annual salary; by 45, it reaches 4x. For a senior manager earning RM12,000 per month (RM144,000 per year), that means RM432,000 to RM576,000 in total retirement savings. This is the decade when the gap between those who are on track and those who are not begins to widen sharply. The most common shortfall at this age is not a lack of savings intent; it is portfolio concentration, specifically, too much in EPF and too little in growth assets like equities or unit trusts.

EPF is not an investment portfolio. It is a secure, tax-advantaged foundation. A professional in their 40s who has RM300,000 in EPF and nothing else in retirement savings is significantly behind the benchmark. The 40s are the decade to build a genuine investment strategy alongside EPF contributions, not simply wait for statutory contributions to accumulate.

Maximising EPF, Reviewing PRS, and Tightening the Insurance Picture

Voluntary EPF top-ups beyond the statutory rate are particularly powerful in this decade. With 15 to 20 years of compounding remaining, every additional ringgit deposited into EPF earns the annual dividend, recorded at 6.15% to 6.30% in the 2024, 2025 period, tax-free. Review your PRS fund’s performance and asset allocation: if the fund has drifted too conservative given your timeline, adjust it. On insurance, the focus shifts from establishing coverage to confirming it is correctly sized as income has grown since your 30s. A RM7,000-per-month earner who last reviewed their life cover when earning RM5,000 per month is now underinsured.

An estate plan, specifically a valid will and updated EPF and insurance nominations, becomes non-negotiable in this decade. Without a will, the distribution of your assets follows the Distribution Act 1958, which may not reflect your intentions and almost certainly creates delays. These are the milestones that separate methodical planners from those who assume everything will sort itself out.

Your 50s: The Final Sprint Before Retirement

The 6x, 7x Target and the Catch-Up Window

By age 50, the benchmark is 6x your annual salary; by 55, it rises to 7x. For a director-level professional earning RM18,000 per month (RM216,000 per year), that translates to a total retirement pot of RM1.3 million to RM1.5 million. This is a significant number, and the reality check at 50 can be sobering. According to EPF 2024 data, the average active-member balance for those aged 50 to 54 stands at RM237,426, and many in this cohort have limited additional retirement assets beyond EPF, placing them well below the benchmark for their salary level.

The 50s offer a narrow but genuine opportunity to accelerate. Income is typically at its highest, children may be finishing their education, and mortgage payments are often nearing completion. The freed-up cashflow in this decade is the single most powerful catch-up tool available. Directing even RM2,000 to RM3,000 per month additionally into voluntary EPF top-ups, unit trusts, or other growth assets over a decade makes a material difference to the final retirement number.

Portfolio Repositioning and Income Replacement Planning

The 50s are the decade to begin a gradual shift in portfolio allocation: from growth-heavy to a more balanced position. The conventional glide path recommended by Malaysian financial planners suggests moving toward 40 to 50% equities and 50 to 60% in bonds, sukuk, or fixed income instruments as you approach 60. This does not mean abandoning growth entirely; a retirement that begins at 60 may extend to 80, giving the portfolio a 20-year horizon that still requires some equity exposure to outpace inflation.

Begin modelling your monthly retirement income stream explicitly. What does the projected EPF dividend income look like on a partial withdrawal basis? What does a 4.5 to 5% annual drawdown from your investment portfolio generate in monthly ringgit terms? Map the gap between this projected income and your 70 to 80% income replacement target. If the gap is visible at 55, it is still bridgeable. At 62, the options narrow considerably.

Your 60s: Converting Your Nest Egg Into a Sustainable Income Stream

The 8x, 10x Benchmark and Your EPF Withdrawal Strategy

By age 60, the savings benchmark is 8x your annual salary; full retirement readiness is conventionally set at 10x by age 65 to 67. EPF allows full withdrawal at age 55 or 60, and the timing and structure of that drawdown matters enormously to long-term sustainability. Withdrawing too aggressively in the first years of retirement introduces sequence-of-return risk: if the market performs poorly in year one or two of retirement, you are drawing down a reduced portfolio, permanently impairing the compounding capacity of remaining assets. Strategy at this stage is not optional; it is everything.

Making the Savings Last Through a 15-to-20-Year Retirement

A sustainable withdrawal rate of 4 to 5% annually preserves capital across most 20-to-25-year retirement scenarios. For an EPF-heavy portfolio, where the fund’s dividend yield of 6.15% in 2025 consistently exceeds Malaysia’s long-term inflation rate of approximately 2.5%, a starting withdrawal rate of 4.5 to 5% is defensible. For a more diversified portfolio including equities and unit trusts, beginning at 4% and adjusting upward only in strong return years is the more conservative and appropriate approach.

Pair this drawdown strategy with EPF dividends on retained balances, tax-free PRS withdrawals available from age 55, and any rental or investment income. Keeping 2 to 3 years of living expenses in near-cash instruments, fixed deposits or money market funds, provides a buffer that prevents forced selling during market downturns. Neither a large EPF balance nor a diversified portfolio automatically produces a sustainable retirement income. The structure must be intentional.

What to Do If Your Milestones Don’t Match the Benchmarks

A Corrective Action Plan for Each Decade

Being behind the benchmark is common. Staying behind is a choice. The corrective steps differ by decade, but the principle is the same: act while the compounding window is still open.

In your 30s, increase your savings rate by even 3 to 5% of income and start PRS contributions immediately to capture the tax relief available until assessment year 2030. In your 40s, redirect every salary increment directly into EPF voluntary top-ups and equity-based unit trusts before lifestyle inflation absorbs it. In your 50s, consolidate fragmented accounts, sell consistently underperforming assets, and replace rough guesses with a real income-replacement projection, one that accounts for your actual spending, healthcare costs, and planned retirement age. These steps apply regardless of how large the shortfall is; they are the same levers, calibrated to the size of the gap.

The benchmarks in this retirement planning milestones by age guide are a diagnostic tool, not a verdict. A shortfall at 45 is not a financial failure; it is actionable information that tells you exactly what needs to change and by how much.

Why a Personalised Stress-Test Changes the Picture

Savings multiples like 3x or 6x your annual salary are powerful as a first filter. They cannot, however, account for your personal variables: lifestyle inflation, a plan to retire at 55 rather than 60, a child’s overseas university fees, ageing parents who need financial support, or a portfolio weighted entirely in one asset class. These are the details that determine whether the benchmark number actually funds your specific retirement, or simply looks adequate on paper.

At CF Lieu, a fee-based financial planner based in Malaysia, a flat-fee, commission-free engagement goes beyond the benchmarks. The process involves building a full retirement roadmap: modelling your actual cashflow decade by decade, stress-testing your EPF and investment portfolio under different market scenarios, and identifying gaps while there is still time to close them. Because the engagement is fee-only, recommendations are driven entirely by your numbers and your goals, not by product commissions. The initial consultation is complimentary, removing the barrier to finding out exactly where you stand before the window for easy corrections closes. This is how it is being done:

The Benchmarks Are Your Map, Not Your Destination

The 45-year-old manager from Petaling Jaya now has a lens through which to evaluate her position. If she earns RM12,000 per month, the 4x benchmark at age 45 tells her she should have roughly RM576,000 in total retirement savings. If her EPF balance is RM280,000 and she has little else, she knows the size of the gap and the decade she has left to address it. That clarity is worth more than any amount of vague reassurance.

The retirement savings targets by age are straightforward: 1x your annual salary by 30, 2x by 35, 3x by 40, 4x by 45, 6x by 50, 7x by 55, and 8x to 10x by retirement. Each is a prompt for action at that specific stage of life, not a retrospective judgement on what has already passed. The professionals who retire with genuine financial confidence are not uniformly the highest earners. They are the ones who checked these milestones early and made adjustments before the compounding window narrowed.

Use this retirement planning milestones by age guide to check your readiness, and if you want to go beyond the benchmarks and build a plan that accounts for your actual life, book a free initial assessment with CF Lieu. A single conversation can tell you whether your current trajectory is sufficient and, if not, exactly what it would take to get there.