Many Malaysians hold at least one life insurance policy, yet according to Life Insurance Association of Malaysia (LIAM) data, coverage levels frequently fall well short of what households actually need, with average sums assured often below what financial planners consider adequate. Most people have never completed a formal insurance needs analysis, and that gap between owning a policy and being properly covered is precisely the problem this guide addresses.

An insurance needs analysis is a structured calculation that tells you exactly what protection you require. It measures what your family would need to maintain their financial position if you died, became permanently disabled, or received a serious diagnosis, then compares that figure against what your existing policies would pay out. The gap between those two numbers is what you are here to find. This guide walks you through the full process: the key variables, two recognised calculation methods, how to match cover types to specific needs, and how to audit your current policies honestly.

This is also the structured approach that independent, fee-based advisors at practices like CF Lieu use when conducting unbiased coverage assessments for clients. Understanding the methodology gives you both the numbers and the confidence to act on them.

Table of Contents

What an insurance needs analysis actually tells you

Many Malaysians hold at least one life insurance policy, yet according to Life Insurance Association of Malaysia (LIAM) data, coverage levels frequently fall well short of what households actually need, with average sums assured often below what financial planners consider adequate. Most people have never completed a formal insurance needs analysis, and that gap between owning a policy and being properly covered is precisely the problem this guide addresses.

An insurance needs analysis is a structured calculation that tells you exactly what protection you require. It measures what your family would need to maintain their financial position if you died, became permanently disabled, or received a serious diagnosis, then compares that figure against what your existing policies would pay out. The gap between those two numbers is what you are here to find. This guide walks you through the full process: the key variables, two recognised calculation methods, how to match cover types to specific needs, and how to audit your current policies honestly.

This is also the structured approach that independent, fee-only advisors at practices like CF Lieu use when conducting unbiased coverage assessments for clients. Understanding the methodology gives you both the numbers and the confidence to act on them.

What an insurance needs analysis actually tells you

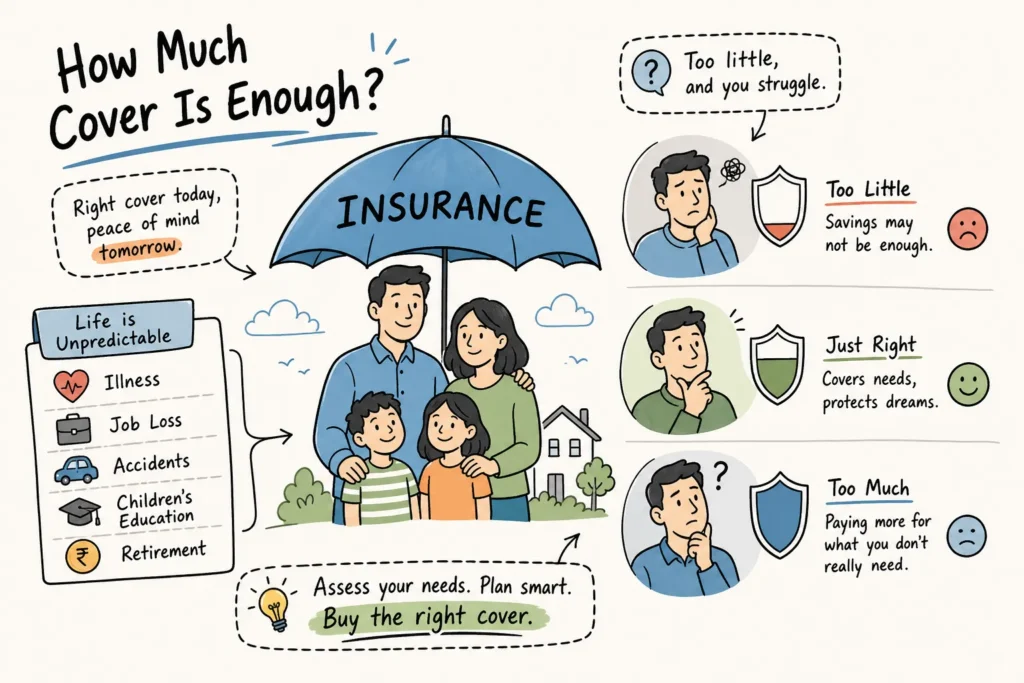

Holding an active policy is not the same as being adequately covered. An insurance needs analysis compares what your family would need financially against what your policies would deliver. The result is your insurance gap: the shortfall between your family’s real requirements and your current sum assured.

This analysis is not just for first-time buyers. Anyone who has taken on a mortgage, had children, or received a significant salary increase since their last review should run the numbers again. Life changes faster than most policies are updated, and the financial consequences of ignoring that gap are permanent.

Malaysian households are frequently underinsured, and a contributing factor is that many buyers focus on premium affordability rather than the coverage amount being purchased. The foundation of any sound analysis is income replacement: if your income stopped today, for how long and at what amount would your family need it replaced? That single question, answered honestly, tends to reveal just how wide most gaps are.

Four factors that determine how much cover you need

Income is the starting anchor of any life insurance needs analysis. The question isn’t simply “how much do you earn?” but “how many years would your family need that income replaced?” The answer depends directly on the age of your youngest dependant and how many years remain until they reach financial independence. A widely used Malaysian industry starting point is annual gross income multiplied by ten as the minimum coverage baseline, a rule of thumb you will also see embedded in most online life cover calculators and insurance needs calculators.

Outstanding debts do not disappear upon death. Your home loan, car loan, personal loans, and credit card balances remain, and banks will move to recover them if they are not settled. Life stage matters equally here: a 35-year-old with young children and a fresh mortgage has fundamentally different needs from a 55-year-old whose children are independent and whose loan balance has halved.

Finally, assets already in place reduce your gross coverage target and must be factored in. EPF savings, unit trust investments, and the sum assured of existing policies all count as resources available to your family. Subtracting these from your gross target produces the net gap your analysis is designed to surface, the true figure this entire exercise is built around.

How an insurance needs analysis uses the DIME method

The simplest and most widely recommended starting point is annual gross income multiplied by ten. If you earn RM120,000 a year, your baseline coverage target is RM1.2 million. This figure accounts for roughly ten years of income replacement, assuming the lump sum is invested at a modest return. It is a useful estimate, but incomplete for households carrying significant debt or with children who need education funding.

For a more complete picture, the DIME method, a recognised capital needs analysis framework, builds a coverage target by summing four specific financial obligations. Work through the components in order:

D, Debt

Add up every outstanding liability excluding your mortgage: personal loans, car loans, credit card balances. These must be cleared so creditors cannot pursue your estate or repossess assets.

I, Income

Multiply your annual take-home pay by the number of years until your youngest dependant reaches financial independence, typically 15 to 20 years for a household with school-age children. This is the income replacement component of your human life value calculation.

M, Mortgage

Include the full outstanding home loan balance. If you already hold a Mortgage Reducing Term Assurance (MRTA) policy that covers this loan, you may exclude it here.

E, Education

Estimate tertiary education costs per child. A widely used Malaysian benchmark is approximately RM50,000 per dependant as a funding buffer for university or college, giving RM100,000 for two children. Local public university fees and private college costs vary considerably, so review current figures and adjust accordingly.

Sum all four figures to produce your gross coverage target. This is not your final answer. Subtract your current EPF balance, existing investment portfolios, and the sum assured of any active policies. The remainder is your net insurance gap, the coverage shortfall your analysis is designed to surface. Work through this with your own numbers and the gap becomes impossible to estimate away.

Matching the right type of cover to each need

Different cover types serve distinct financial functions and cannot simply substitute for one another. Term life insurance is the most cost-efficient solution for temporary needs tied to a specific debt or dependency window, such as a 20-year home loan or raising children through university. TPD (total and permanent disability) cover complements term life by addressing the scenario where you survive but can no longer generate an income. This situation can be more financially damaging than death, because living expenses continue while earnings stop entirely.

Trauma insurance, also known as critical illness cover, pays a lump sum upon diagnosis of specified conditions such as cancer, stroke, or heart attack. It funds treatment, recovery, and lifestyle adjustments that neither life insurance nor TPD cover addresses directly. Income protection, by contrast, replaces a percentage of your monthly salary, typically 50 to 70 per cent, during an extended period of illness or injury.

A complete insurance needs analysis should assess all four layers: term life, TPD, trauma, and income protection. Relying on a single life policy leaves three of those gaps entirely open, which is precisely why so many Malaysian families face financial crisis following a serious diagnosis even when they believed they were covered.

Insurance needs analysis: audit your policies step by step

Pull out every active policy and ask four questions of each one: What is the current sum assured? When was it last reviewed? Does it still reflect your outstanding mortgage balance and current income? Is the beneficiary nomination current and accurate? Many Malaysians find that a policy purchased in their late twenties now significantly underfunds the life they have built a decade later.

On the estate planning side, Malaysia has no estate tax, but an improperly nominated policy becomes part of the estate. This delays the payout and generates administration costs your family must absorb at the worst possible time. Keeping nominations up to date ensures proceeds pass directly to your intended beneficiary without being held up in probate or administration proceedings. If you are unsure how to document nominations and preserve assets, read guidance on how to really write a fool-proof personal will for asset preservation.

The most frequent coverage gaps tend to follow recognisable patterns: no income protection layer at all, TPD cover too low to fund long-term care, a sum assured fixed at policy purchase and never increased alongside income growth, and no trauma cover despite the substantial financial risk posed by critical illness. Pre-retirees face an additional risk: employer-provided group life and medical cover typically ends at age 60 with no conversion offer, yet the average Malaysian lives to 75 to 77 years. That 15-year gap demands active planning rather than the assumption that existing policies will carry forward. For a practical look at coverage across different life stages, see this life insurance coverage at each stage of life summary.

When a professional second opinion is worth the investment

The DIME method gives a solid directional answer. The calculation is only as accurate as the assumptions behind it, however, the investment return assumed on the lump sum, the education cost projections, and whether the cover types selected actually match the policy definitions in the fine print. Most people never read the exclusions carefully, and some policies that appear to provide TPD or trauma cover use definitions far narrower than expected. A figure that looks adequate on paper can unravel entirely when a claim is tested.

CF Lieu’s flat-fee insurance review service is a practical option for anyone who has completed their own analysis and wants an independent expert to validate or challenge it. Because the advisory model is entirely commission-free, no recommendation is influenced by product incentives or sales targets. The review assesses whether your current sum assured and cover types genuinely align with your life stage, liabilities, and income profile, providing the kind of second opinion that gives real confidence before committing to changes.

For high-income earners, executives, or anyone with multiple policies accumulated over the years, this structured audit frequently reveals consolidation opportunities and coverage overlaps that more than justify the advisory fee. It can also reveal cost saving opportunities such as this client case study. The goal is not to sell you more insurance; it is to make sure every ringgit you are already spending on premiums is doing the job you think it is.

The next step after running your numbers

An insurance needs analysis is not a one-time calculation done when you first buy a policy. Income grows, mortgages are taken on, children arrive, and life stages shift, each of these events changes the coverage equation entirely. The practical step today is to work through the DIME calculation with your current numbers and compare the result to what your policies provide.

If the gap is significant, act sooner rather than later. Premiums increase with age, and a health event can make cover harder to obtain on reasonable terms. For more context on why premiums and healthcare costs tend to rise over time see why healthcare costs & insurance premiums are bound to increase. If the numbers look reasonable but you want certainty, a professional, unbiased review can confirm whether your coverage is genuinely adequate or simply close enough to feel comfortable. Gathering your salary slips, mortgage statement, EPF balance, and existing policy schedules typically takes under an hour, and that hour of preparation is one of the most valuable financial exercises any Malaysian breadwinner can complete.

Ready to find out precisely where your coverage stands? Book a free initial consultation with CF Lieu to review your current policies, calculate your real coverage gap, and get independent advice on the right next step for your situation.

FAQs: Insurance Needs Analysis that actually matters

What is an insurance needs analysis and why is it important?

An insurance needs analysis is a structured calculation that compares what your family would need financially if you died, were permanently disabled, or received a serious diagnosis against what your existing policies would pay out. It identifies the insurance gap—the shortfall between real requirements and current sum assured—so you can take targeted action rather than just holding a policy that may be inadequate.

Why are many Malaysians underinsured despite owning life policies?

LIAM data shows average sums assured frequently fall short of household needs because many buyers prioritise premium affordability over coverage amount and few complete a formal analysis. Life changes like mortgages, children, or salary increases often aren’t reflected in older policies, widening the protection gap.

What are the main factors that determine how much cover I should buy?

Four key factors are your income (and how many years it needs to be replaced), outstanding debts (home loan, car loans, credit cards), your life stage (age of youngest dependant and remaining dependency years), and assets already in place. Combining these produces a gross coverage target from which you subtract existing resources to find the true shortfall.

What is the DIME method and how is it used in an analysis?

The article presents DIME as one recognised calculation approach and highlights the simple, widely used starting point of annual gross income multiplied by ten as a baseline. For example, earning RM120,000 a year sets a baseline target of about RM1.2 million, which you then adjust for debts, dependants, and existing assets to find your net gap.

How often should I re-run an insurance needs analysis?

You should re-run the analysis after material life changes—taking on a mortgage, having children, receiving a significant salary increase, or any event that alters your dependants or debts. Because life often changes faster than policies are updated, periodic reviews ensure your coverage remains adequate.

How do I calculate how much life cover I need?

Start with an income-replacement anchor (a common Malaysian baseline is annual gross income multiplied by ten) and add outstanding debts and future expenses tied to life stage. Then subtract assets available to your family—EPF savings, unit trust investments, and existing policy sums assured—to reveal the net insurance gap you must fill.

How do I audit my current policies honestly to find the gap?

List the sum assured for each existing policy and compare the total against your calculated gross coverage target, then subtract assets like EPF and investments to determine the net shortfall. An independent, fee-only advisor (the article cites practices like CF Lieu) will use this structured approach to provide an unbiased assessment if you prefer professional help.