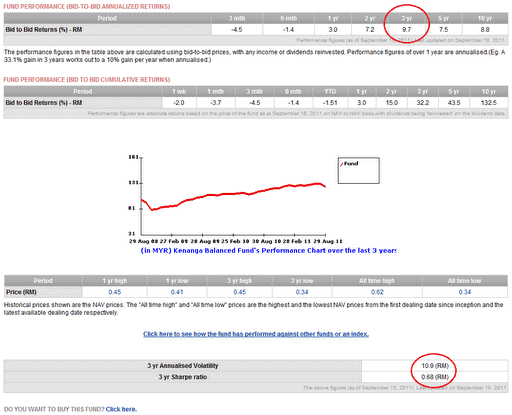

The Sharpe Ratio of Unit Trust – a method to estimate its risk return profile.

In any financial investment, risk and return go in parallel. Guaranteed return is known as risk-free return, and almost always refer to either Fixed Deposit rate or Malaysian Government Securities coupon rate. If you are buying government bond such as Greece, it is no longer risk free anyway! FD rate seldom goes beyond 4%; here’s a summary of the current risk free rate of return (FD).

Sharpe ratio of an investment refers to how well the investment generates a return taking into consideration the risk. Risk is high when the investment nature has high volatility – tendency for its value to soar or to plunge excessively within a specific timeframe when benchmarked against the overall market activity.

For the mathematically inclined, the equation is as such:

Sharpe ratio for Investment Z = (Investment return for Z – Risk Free Rate of Return) / Standard Deviation for Investment Z

High volatility = High Standard Deviation

Sharpe ratio –> Higher is better.

Taking Risk Free Rate of Return as constant, 2 factors contribute to higher Sharpe ratio

- Higher investment return

- Lower volatility