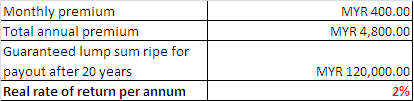

In Excel, use the formula: Rate(20,4800,0,-120000) and you get 2%.

And she further illustrates that an engineering degree currently costs about RM 150,000, with the assumption that the cost for college doubles every 10 years.

I do not know how she came up with RM 150,000; but it could not be anywhere in Malaysia’s local public or private institutions. An engineering degree at Multimedia University, my Alma mater, is currently tagged at RM 50,000. Therefore, let’s take this as baseline for calculation below. Overseas education are really, the privilege of the rich, and they are not any man on the street like the rest of us. Moreover, there are factors such as exchange rate fluctuation which we could not anticipate in the future, so let’s be realistic and keep things simple.

*assume the cost for college doubles every decade

Second key takeaway here: Endowment plan payout in 20 years can only fulfill one third of your child’s college cost plus living expenses in the same timeline.

Now, the contributor advocates properties investment but I am not going into details of her plan here although it is very ideal if you have the cash for at least 10% down payment of the properties value, plus other closing college costs. Whatever the investment vehicle, everyone has their own preference. Just be prudent to balance the risk versus return.

Anyway, below are my estimation of the investment needed now to cover education cost of RM 370k.

Save Now, Create Later

If anyone starts to allocate RM 10k today into investment vehicle of your choice with moderate return of 6 percent per annum, with yearly top up of RM 9.6k, he or she will be able to cover his/her child cost for college in 20 years.

RM 9.6k per year translates to setting aside RM 800 per month, with father and mother each contributing RM 400. Do-able right?

And you still have surplus of RM 14k, which can be used as down payment for your child’s first car when he or she starts working after graduating.

Bear in mind this is only for one child. What if…

a) You have more than one child?

b) You child desire to study medicine, and he/she is capable of – you don’t want to kill their dreams right?

Securing a scholarship though, is an added bonus. But I will only using EPF Account 2 for children college costs as last resort, because it will surely jeopardize my retirement plan.

The Downside of Active Self Investment

There is no insurance element in it, unlike endowment plan. The insurance component of endowment plan will provide the insured amount compensation to the proposer (parent) in the event of death or total permanent disability of the child. I do not think this is critical. On the other hand, if the proposer passes away/permanently disabled/suffers from any of the 36 critical illlness, the policy will sponsor the child until maturity.

To mitigate the risk of parent not able to provide financially to their child, any parent should be sufficiently insured. Like my previous CFP facilitator mentioned, if you love your family, and being the primary income earner, you should buy more insurance for yourself, NOT for your spouse/children.

Disclaimer: I am not an insurance agent.

Who am I?