This is perhaps most comprehensive guide listing the costs of medical treatment/procedures in Malaysia.

The best part?

Read more below to discover a full list of medical procedures costs published by Ministry of Health (Federal Government Gazette) known as Private Healthcare Facilities & Services (Private Hospitals & Other Private Healthcare Facilities) Amendment Order 2013.

Last but not least, if you want to correlate the costs of medical procedures with the rationale of getting a medical insurance, you’ll love this write-up.

Let’s get started

As Malaysia progresses towards becoming a high-income status nation by the year 2020, the cost of living in the country will inevitably increase exponentially and the costs of medical procedures will also rise in tandem.

What is medical inflation? What is the medical inflation rate?

Medical inflation is evolution in medical trends and developments, and the continuous uptick in cost to support them. This often includes the cost of advances in treatments and procedures, and the increased availability and usage of them.

Medical inflation in Malaysia has been estimated to increase to about 10 to 15 percent annually, 2x – 3x higher than inflation for cost of living and based on statistics from the past 15 years, the medical inflation rate has increased by a whopping 107 percent.

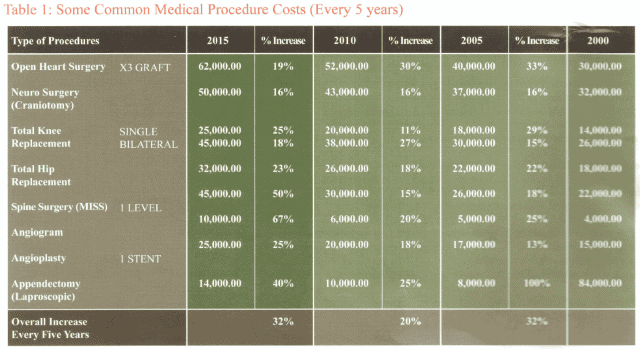

Over the course of 15 years, the costs of medical procedures have almost doubled. For example, an open heart surgery used to cost only RM 30,000 in 2000, but in 2015, its cost has more than doubled to RM 62,000.

Similarly, the cost of a single total knee replacement surgery was only RM 14,000 in 2000, but has increased to RM 25,000 in 2015.

A craniotomy, meanwhile, used to cost RM 32,000 in 2000 but has increased to RM 50,000 now.

Angiograms and one-stent angioplastics used to cost RM 4,000 and RM 15,000 respectively back in 2000. Now, the price of these procedures has risen significantly to RM 10,000 and RM 25,000.

| Cancer Illness Type | APPROXIMATE TREATMENT COST AT PRIVATE HOSPITAL(RM) | ESTIMATED TREATMENT COST AFTER 10 YEARS (RM) |

|---|---|---|

| Breast Cancer | 18,000 – 395,000 | 62,000 – 1,353,000 |

| Colorectal Cancer | 36,000 – 121,000 | 123,000 – 414,000 |

| Lung Cancer | 45,000 – 56,000 | 154,000 – 192,000 |

| Cervical Cancer | 20,000 – 60,000 | 68,000 – 205,000 |

| Nasopharyngeal Cancer | 22,000 – 70,000 | 75,000 – 240,000 |

Medical Costs Difference between Private vs Public Healthcare in Malaysia

| Medical Treatment | Private Hospital (up to) RM | Public Hospital (average) RM |

|---|---|---|

| Angioplasty | 40,000 | 200 |

| Cataract | 6,000/eye | 500 |

| Chemotherapy | 4,000/cycle | 200/visit |

| Dengue | 3,000 | FOC |

| Heart Bypass | 80,000 | 4,000 |

| Hip Replacement | 50,000 | 15,000 |

| Kidney Stone | 40,000 | 10,000 |

| Spine Surgery | 50,000 | 36,000 |

| Stroke | 70,000 | 5,000 |

(Note: figures are estimated, if you think they are wrong, comments below)

Hospital Service & Supplies Charges Difference between Private vs Public Healthcare in Malaysia

| Type of Charges | Private Hospital (up to) RM | Public Hospital (average) RM |

|---|---|---|

| Ambulance Fees | 200 | 50 |

| Consultation Fees | 250 | 1 |

| CT Scan | 1,000 | 450 |

| Angiography | 2,500 | 75 |

| Blood Test | 100 | 1 |

| General Anesthesia | 1,000 | Free |

| MRI Scans | 1,200 | 700 |

| X Ray | 80 | 1 |

| Ultrasound | 300 | 100 |

(Note: figures are estimated, if you think they are wrong, comments below)

For official long list of medical procedures and how much it costs, head over to this link by Ministry of Heath.

Or watch this video. This will pretty much answer your question:

How much does it cost to see a doctor in Malaysia? Are hospital bills expensive?

The medical fee schedule spells out the maximum allowable fees charged by the medical profession for consultations and procedures, such as cancer treatment (like prostate or breast cancer). It is very different from other professional fee schedules like the lawyers which spells out the minimum fees to be charged.

Do note, however, that the bulk of medical fees for hospitalization comprise hospital charges (services and supplies) which remain unregulated to date.

The killing part is NOT the one-off fees like surgery, blood test, health screenings or other in-patient charges.

The killing part is usually the medical conditions which require recurring treatments, such as various forms of cancer.

Chemotherapy for cancer patients comes in a variety of forms, but unfortunately, they’re all pretty expensive. Even in government hospitals, you’re looking at RM50-200 for each cancer treatment. For private hospitals, they can range from RM170 per day, all the way up to RM1030 per cycle, and that’s not including daycare rates, which range between RM30-RM100 a day.

Then there is this take-home drugs, which aren’t any cheaper. While you do save on daycare, these scary pills can cost as much as RM500 a pill, sometimes even more. Imagine taking one every day for a month, and you’re getting an idea of how expensive chemotherapy can become.

The Crux of Widespread Concern

The unstoppable increase in health spending has raised the question of whether the private healthcare system is sustainable in the long term as patients who pay out of pocket will soon find private medical health care out of their reach. When compared with other countries in AsiaPac region, Malaysia’s healthcare expenditure is expected to reach up to U$ 681 per capita by 2018. This indicates that Malaysia is expected to have higher healthcare spending, which in turn reflects the increase in healthcare cost in the near future.

In the coming years, the healthcare industry, will be one of the top growth sectors. This is because is it driven by rising affluence of communities as well as growing number of middle income citizens who have better private health insurance coverage. The rising cost of treatment in private healthcare can also be attributed to the rising demand from patients who require better healthcare system and services. There is a huge growth expected over the years particularly for the lower middle-income bracket.

Even though a person can be healthy, ailments can happen unexpectedly due to old age. Yet, none of us are likely to include major hospitalization bills or expensive medical treatments in our blissful retirement vision. But an unexpected turn of events such as terminal illness or accidents can easily wipe away all your life savings.

There is no question that healthcare expense is a big concern for retirees. In fact, many studies suggest it is the biggest concern that retirees have. Instead of planning ahead, many find ways to limit their spending during retirement years as a way to mitigate the worst of health circumstances.

If you are not convinced and wonder how does medical cost inflation in Malaysia compare to other countries, check out the below:

Why do costs of medical procedures continue to rise?

- Private healthcare operators boast some of the most state-of-the-art equipment available in the market. A good example is the use of X-ray machines decades ago, which have now evolved to more high-tech equipment like MRI scan or CT scan. In order to purchase and maintain these new equipment, medical costs will naturally rise. To operate these advanced equipment, hospitals need to hire better qualified staff who require higher wages, which can go up by double the standard amount, naturally increasing cost at all points.

- Demand for more resources and basic needs such as healthcare as country’s population continues to grow. By 2018, it is projected AsiaPac region will consist of more than 2.3 bil people above the age 65. Aging population will require long term medical services and medication, naturally escalating the costs of healthcare.

- Life expectancy of Malaysians has seen a steady increase since 1960s. An average age for a man in the 60’s was only 52 years while for women, 55. In the 80’s, it has increased to 65 and 68. Two decades later, the age for men averaged 72 while for women, 76.

- Lifestyle diseases due to sedentary lifestyle & hectic work schedule have become a common, such as coronary heart disease, stroke, influenza and pneumonia, HIV/AIDS, tuberculosis, lung cancer, diabetes mellitus, lung disease, kidney disease and colon cancer.

- Blame game between insurers and private hospitals

Obstacles faced by healthcare industry

Main one is shortage of qualified and specialized medical staff and medical professionals. It’s not about the numbers since private colleges offering medical courses are mushrooming nowadays. It’s about really competent medical professionals, not just paper qualification. That aside, the doctor to patient ratio stands at 1.:791, and in 5 years from now, based on estimated population of 34 mil, the average ratio should be 1:400.

Second is the ever increasing costs of specialty drugs. Presently, there is no cap for price of pharmaceuticals, which could be one reason for the hike. Additionally, the rising cost of specialty drugs could also be attributed to the increasing rate of raw materials, equipment, labour and also the weakening of Ringgit. Although the Health Minister said that the implementation of GST on April 2015 will not affect the health care industry, the various by products used in healthcare services are not exempt and this has increased costs quite significantly.

The rising costs of healthcare is inevitable in anywhere around the world. Private healthcare serves as a means for people who wants to avoid the long waiting times and reduce the burden of overcrowding public government hospitals.

So what can we do as consumer? The smartest option is to plan for private insurance that allows individuals to seek treatment in both public and private medical facilities at later stages of life. Medical costs is one of the most overlooked matters in retirement planning. In the long run, the best way to manage costs is to practise financial planning and ensure there is adequate savings to cover medical emergencies.

How to minimize financial impact due to rise in the costs of medical procedures

Don’t wait till you’re sick

Health problems do not discriminate between age and gender. Those who have been known to lead the healthiest of lifestyle could also fall prey to unexpected, life-threatening diseases.

For those who are planning for retirement, healthcare is a huge expenditure to plan for on top of normal living expenses. Unlike travel, hobbies or entertainment expenses in retirement, medical expenses are non-discretionary. If you are sick or injured you need treatment. Having adequate reserves and a good medical coverage can be the difference between a comfortable retirement and one filled with financial challenges.

It is critical that you take a hard look at what your medical expenses might be and factor these costs into your retirement spending estimation as well.

The key product solution for healthcare protection is medical insurance covering critical medical conditions. While people are generally encouraged to start protecting their health at an early age, it is never too late to start tending to your well-being.

But don’t wait till you are sick as medical insurance is only available to those who are in good health because insurance company is required to underwrite one’s risk. Also, the older you get, the more insurance is likely to cost.

The biggest chucks of healthcare costs

As retirement planning needs to be personalised, so is planning for your healthcare cost in retirement as different people will have different health risk factors. As such, it pays to look into your family health history to determine your health risks in order to prepare more adequately towards it.

According to the World Health Organization (WHO), the top killer diseases in Malaysia are coronary heart disease and stroke. There are treatments for these diseases and other critical illnesses but they don’t come cheap. To make matters worse, medical costs are getting higher by the year as our health deteriorates with age. In Malaysia, the medical inflation rate, which is the increase of medical costs, is between 10% and 15% every year.

For instance, medical treatment for cataract costs RM3,500 to RM5,000 now and in 20 years, it could rise to between RM24,000 to RM34,000.

Long term assisted care

Another thing most-overlooked is medical long-term assisted care in a nursing home at their last stage of life. This is so that their family members don’t get burdened with the hassles of taking care of them.

• Home care – for those who are more independent but need a bit of home care.

• Day care – for those who are lonely at home, day care provides interaction with other senior citizens.

• Integrated residential care centers or IRCCs – for those who had a bad fall or are bedridden and will need more care and rehabilitation care.

• Dementia care – for those Dementia patients who need a home where they can walk around, socialize and perform daily tasks in a safe and secure environment.

Long-term care facilities can range from RM1,000 a month with basic care services in semi-private room to RM5,000 a month, in a private room with skilled nurses and in-house doctors providing professional and specialised healthcare for rehabilitation or palliative care. In the United States, four out of every ten people who reach the age of 65 will enter a nursing home at some point in their lives.

About 10% of the people who enter a nursing home will stay there five years or more. In Malaysia, we need to account at least a year stay in a nursing home and it is wise to factor in a 10% a year medical inflation if you are planning ahead for the future.

Planning a smooth sunset ride

It is important that we face our sunset years realistically. While critical illness like stroke or cancer can be fatal, one’s quality of life can certainly be enhanced with adequate medical attention. One of the surest way to address your concerns in the face of medical catastrophe is by getting an insurance policy that will see you through your medical needs.

Here are a few things to note when shopping for medical insurance policy.

• Get a medical insurance when you are in good health.

• Average lifespan of Malaysians is 75, so ensure plan provides protection way beyond that.

• Look for plans that do not impose a fixed lifetime limit to ensure continuous and uninterrupted access to medical care you may require in your old age. Consider an unlimited medical coverage that starts over every year, regardless of the amount of claims you have made previously.

• Look for a higher annual limit to help cope better with escalating medical costs.

• Lastly, never ignore the fine print that is almost always at the edge of your documents. Make sure your insurance provider does not impose a co-insurance policy on you, meaning you will have to pay a certain percentage of the hospital bill on your own.

For long-term nursing care, because it is highly unlikely covered by your medical insurance, you would have to actively set aside an amount to be invested to grow this fund.

There is no denying that healthcare costs are a major concern and even bigger expense for most retirees. But a financially successful retirement plan that includes a combination of proper health insurance coverage to provide the necessary medical attention when one gets sick and additional provision for long-term care will definitely set you on a correct path to a solid retirement plan.

Last but not least, if you are not a Malaysian citizen (whether you are from South Korea/Costa Rica/Hong Kong/Saudi Arabia/South Africa), know that Medical tourism is a big thing in Malaysia because the country have lots of world class healthcare facilities. However, you only get to enjoy this if you possess a Health insurance plan, formally known as hospitalization and surgical insurance or casually known as medical card, provides for medical expenses incurred due to illnesses.

SOURCE: INTERNATIONAL LIVING MAGAZINE

Adapted from an article in 4E Journal 4Q 2015 published by FPAM, written by CEO of Ara Damansara Medical Center, Sue Lee, CFP.

Reference: Article from RinggitPlus and article from Cilisos

wtfish…the article is about the rising price of healthcare but nobody cares about it..and why in the world all the insurance agent has the gut to sell their insurance here…regardless…quite narcissistic should I say.

i wont be surprise on how ignorance those insurance agents can be. still remember the passed-away of a Malaysian comedian at a young age on 2020, and yet some of those self-centered agents use that for their marketing materials. yes their message is important (to always be prepared at early stage, bla3), but still….

has a bad experience yourself Amin?

Why is it narcissistic!? If there is no insurance agent to push and motivate people to buy insurance, you think you will walk into the insurance branch and sign up a plan!??? They are doing their job with a purpose which is ultimately to protect each person financial interest. As for the commission, to each job and business there is a PAY DAY. Why do insurance agent gets paid so much is because there is still alot of people like you who thinks insurance is a waste of money and speaks too loud and testing FATE.

allianz insurance call han [censored]

Hi, is it true that the max fees stipulated in 13th schedule of the Act are strictly adhered to? And is it true that insurers will only reimburse us up to the max fees in the 13th Schedule?

Prudential offered to reimburse me RM 20+ k as total fee for a 4 surgeon teams in a 36 hours surgery involving removal of sacrum and insertion of a titanium implant. My son did the surgery in Singapore General Hospital and the total surgeon fees was SGD 85k. Rm 20+ k for such a major and uncommon surgery seems ridiculously low.

SC Yap, let’s just say there’s very little room for negotiation in such scenario you are facing.

Because in any insurance quotation or policy book, this clause is almost standard for hospitalization and surgical coverage benefits (medical card):

If the Life Assured elects to or is referred by the attending Physician to be treated outside Malaysia, the benefits in respect of the

treatment shall be limited to the Reasonable and Customary Charges that are Medically Necessary for such equivalent local treatment

in Malaysia and shall exclude the cost of transport to the place of treatment.

Call me at 0122388948 Eric Wong. I am the claim staff attended to your appeal. I have crucial information for you regarding your son claim.

Hi if you’re interested to know more about income replacement, retirement planning and healthcare benefits, contact me at 0109328407 (Kota Kinabalu)