How do I check my CCRIS? Or

How can I get a CCRIS report in Malaysia?

How do financial institutions evaluate your loan application or credit profile or credit history?

Most importantly, why are YOU being Rejected?

And just so you know, this is the most practical, highly actionable guide on the planet on “CCRIS Check Online” or “Semakan CCRIS / CCRIS Semakan.

The best part?

We are going to shed light on how to turn your loan or credit application from REJECT status to APPROVED.

And how CCRIS (Central Credit Reference Information System), a system that records personal credit rating of Malaysians, really works.

In short, if you want to solve your CCRIS issues, this guide is your best chance. All secrets on CCRIS check are exposed right here.

Let’s get started.

(with over 300+ questions & answers in the comment section below this article, you surely will find the most relevant answer to your questions. So make sure you stick around and don’t leave this CCRIS guide before you read everything in the comments section)

What is CCRIS

CCRIS (central credit reference information system) is a centralized system under Bank Negara that compiles data on your outstanding loan amount and payment history for the past 12 months, at any given time.

Any repayment records older than 12 months are “deleted”.

If you are late in payment (let’s say 6 months outstanding in Feb 2015) but you have paid off the outstanding in March 2015, the records will still show February = 6 months, March = 0 months, April = 0 months.

As CCRIS is a report for a 12 month period, the 6 months in arrears records will only ‘disappear’ in February 2016 (12 months later). You just cannot erase or request to clear it before that, as it is a rolling report.

If it shows, for example, 2 2 2 2 – -, meaning your loan has been due for 2 payments for 4 months.

Everyone has their personal credit report in the form of a CCRIS report which can be retrieved by financial bodies and by the individual himself, but not by other people.

In other words, your eligibility for a loan has nothing to do with how well you know your banker (although that *might help?).

The Credit Bureau is a legally empowered credit reporting agency under CREDIT REPORTING AGENCIES. ACT 2010 to collect personal credit information about you from these financial institutions.

However, the Credit Bureau simply collects and reports your credit information as it is.

In other words, the Credit Bureau does not “judge” your creditworthiness. Also in all fairness, information on rejected credit applications is not reflected in credit reports so that one bank will not be biased by the prior decision of another bank.

Your CCRIS information could in fact be treated differently and subjectively by each financial institution.

Currently, there is an arbitrary limit for the public to print their own report – it can only be done once every three months.

How to conduct your CCRIS check

According to the BNM’s website, there are only 5 locations in Peninsular Malaysia (Penang, Johor Bahru, Kuala Trengganu, KL and Shah Alam) and two locations in East Malaysia (Kuching & Kota Kinabalu) for the public to print their CCRIS reports to get info on their credit information. If an individual is located in Melaka or Ipoh, they would need to go to BNM’s HQ to get and print their credit information reports.

Steps on how to conduct your CCRIS online check F.O.C.

- Go to CCRIS kiosk at Bank Negara Malaysia

- Use your MyKad for fingerprint verification

- Print the report.

An alternative way to do CCRIS check online and resolve CCRIS problems, without stepping out from your house or office – get your CCRIS report in 30 minutes even during non-office hours, weekends or public holidays.

Get the instructions guide (in the short online mini-course) below [CLICK to access]

We will send you the access link after payment.

1a. Do 1-click payment HERE OR…

1b. Pay RM 19.90 using JomPAY via your online banking – Biller Code: 39222

- Send proof of payment to by using this Google form

- You will usually get your the access link within 1 working day – via email so check your email inbox

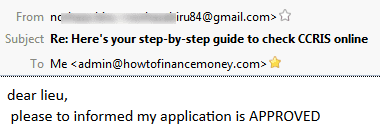

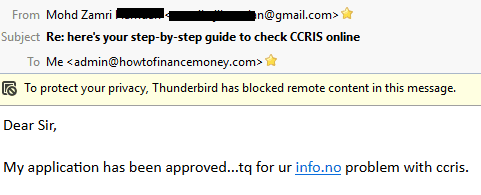

Testimonials from people who bought this Guide and used it to resolve their CCRIS issues

Any other way to do CCRIS check F.O.C. without ever going to BNM?

Unfortunately, no.

Financial institutions’ credit officers are able to access the applicants’ CCRIS report from the comfort of their offices while the public has to drive all the way to Bank Negara or its branches just to do the same, at least to do first time activation.

Doing CCRIS check via email – there’s this thing called eCCRIS BNM.

What is eCCRIS? How do I register with eCCRIS?

- One-time registration by walking-in to BNM HQ or any BNM/Agensi Kaunseling dan Pengurusan Kredit (AKPK) branch nationwide.

- Verify identity using MyKad and register valid mobile phone number at CCRIS kiosk.

- A 6-digit PIN will be sent to registered mobile phone number.

- First-time login at eccris.bnm.gov.my keying in MyKad number and 6-digit pin.

- Set preferred user ID and password, personal security image and phrase, and 3 security questions.

If you are staying out of the BNM branches, you may request your credit report via mail, just complete and send them the application form together with the required documents and fax/send to them. Please note that it may take 2 to 4 weeks to process your request for a credit report via mail. The report will be sent to the nearest financial institutions to your home address.

Step 1: Type in BNM CCRIS [e-mail address] in the textbox, then Send SMS to 15888. RM0.20 will be charged

Step 2: Check your inbox or Spam folder, a form is attached.

Step 3: Print out and complete it

If you want fast and convenient to do a CCRIS check online without going to BNM – follow the instructions above.

How to Read your CCRIS report

*This is based on my own account of doing CCRIS check and getting a report from Bank Negara Penang

This is what the CCRIS report printout looks like. Any BNM branch uses color printer?

- OUTSTANDING CREDIT vs APPLICATION FOR CREDIT.

- The report is divided into two main areas i.e. the Outstanding Credit, where it displays all your existing credit facilities, and the Application For Credit, which shows all the loan application you made in the past 12 months, whether it was Approved, Pending or Rejected by the bank.

- STATUS

- Indicates the status of the credit facility. Outstanding i.e. on-going facility. Other terms include Pending, Approved, Rejected, Settled, Write Off, Rescheduled, or Restructured.

- CAPACITY

- Indicates the capacity the borrowing you took from the bank i.e. as a <Own> own applicant, <SOLE> sole proprietor, <PARTNER> partnership, <JOINT> joint application, <GUARANTOR> acting as a guarantor.

- LENDER TYPE

- Indicates the exact financial institution you borrowed from.

- NATIONALITY

- Indicates whether you are a Malaysian applicant or foreign applicant.

- FACILITY

- Indicates the type of facility enjoyed with the various banks. Includes Overdraft, Housing Loan, Hire Purchase for scheduled goods, Leasing facilities, Staff Loans, Other Term Loans including personal loans, Credit Cards, etc.

- TOTAL OUTSTANDING BALANCE (RM)

- Indicates the outstanding loan amount of other credit facilities at current date.

- DATE BALANCE UPDATED

- The date where information on existing credit facilities is updated to BNM system.

- LIMIT (RM)

- The original loan amount approved, or if revolving credit facilities (such as credit cards or overdraft), the limit assigned for the credit facility.

- PRINCIPAL REPAYMENT TERM

- Whether the repayment frequency is Monthly, Quarterly, Annually, Revolving, or other frequencies.

- COLLATERAL TYPE

- Indicates the collateral type used by the bank to secure your credit facility. Includes <00> Clean facilities (no collateral), <10> Properties, <23> Unit Trusts, <30> Motor Vehicles, <60> Plant and Machineries, <70> Financial Guarantees, etc.

- INSTALLMENT IN ARREARS FOR THE LAST 12 MONTHS

- Most IMPORTANT part of the report, where the track record of conduct for each credit facilities for the past 12 months are indicated.

- If it is indicated as “0” under January, it means your installment for January is paid before due date. If “1”, it means your instalment is 1 month in arrears (overdue) in January, “2” means 2 months instalment overdue in January, “3” means 3 months overdue and considered delinquent, etc.

- If there are too many “2”s and “3”s and/or above, your conduct of credit account may be considered as “poor paymaster”, according to each bank’s interpretation.

- LEGAL STATUS

- Indicates the legal action status of your account if it is in default. The bank can know the action taken such as <10> Summon/Writ files, <11> Judgement Order, <12> Bankruptcy, <17> Winding Up order, <18> Auction, <20> Receivership / Section 176, <12> Settled / Discharged, etc.

- DATE STATUS UPDATED

- Shows the date of latest update on the legal action status.

Disclaimer on CCRIS records/report:

THE INFORMATION CONTAINED IN YOUR CCRIS REPORT HAS BEEN COMPILED FROM THIRD PARTIES AND DOES NOT REPRESENT THE OPINION OF BANK NEGARA MALAYSIA OR ANY REPORT PROVIDER LIKE CTOS OR RAMCI (RAM Credit Information) operating under CREDIT REPORTING AGENCIES. ACT 2010 AS TO YOUR CREDIT WORTHINESS. HENCE, BANK NEGARA MALAYSIA OR ANY REPORT PROVIDER CANNOT ASSUME ANY LIABILITY WITH RESPECT TO THE ACCURACY OR COMPLETENESS OF THE INFORMATION. THE INFORMATION CONTAINED IN THIS REPORT IS SUPPLIED ON A CONFIDENTIAL BASIS TO YOU AND SHALL NOT BE DISCLOSED TO ANY OTHER PERSON.

How is CCRIS report being updated?

After discussing on how to do your own CCRIS check, we now want to know how the CCRIS report is being updated.

In fact, CCRIS information is updated on the 15th of every month. So if you have paid down your credit lines anytime from 1-31 Jan, time your loan application submissions on the 16th of Feb.

In practice, issues crop up impacting consumers when the banks are delayed in updating their customers’ credit facility records to the CCRIS in a timely manner, despite the fact that the banks are supposed to do so on the 15th of each month.

Banks do have problems with their core banking systems (breakdowns, delay, heavy traffic, unable to close the end-of-month due to adjustments in accounts, etc) so there may be reporting delays.

Also, some banks default their system to classify a loan as due at different dates. Some banks classify the instalment due after 5 days, 7 days or on the due date itself, depending on bank policy. This will all affect the bank’s reporting to its risk department. If a bank classifies it as overdue 1 day after the due date, 80%-90% of customers will be on the due report for the Bank’s collection team. Usually, a grace period is given so that the report that the collection team gets is shorter and easier to manage.

In short, whatever comes out in the CCRIS report will depend on how fast your bank report the account to CCRIS, as BNM only compiles whatever that have been reported to them.

Frequently asked questions

How do I check my CCRIS online for free?

Register yourself at BNMLINK Kuala Lumpur oru003cbru003eBNM Offices or AKPK branches. Then do first-time login at https://eccris.bnm.gov.my

How do I get my CCRIS pin?

You must register first at BNMLINK Kuala Lumpur or other BNM Offices or AKPK branches.

What is Special Attention Account?

Loans reported under Special attention Account are loans that are non-performing loans (NPL) that the financial institution has placed under special monitoring in view of recovering the loan or in the midst of collection. Loans under special debt management schedules such as negotiated by AKPK will also fall under here.

It could be due to dishonoured/bounced cheque incidents too.

You definitely don’t want to be ‘special’ when it comes to debt management and CCRIS report.

What can bank see when it check my CCRIS report?

Generally, when a Bank conduct a CCRIS check, they will have access to various credit reports such as:

- Summary Credit Report – Information on the total credit exposure and conduct of account of the customer

- Detailed Credit Report – Information on the specific outstanding credit facilities and new credit applications of a borrower

- Motor Vehicle Report – Information of motor vehicles which are used as collateral for credit facilities

- Customer Supplementary Information Report – Information on the addresses, telephone numbers, employers names and occupation of the customer for the last 3 years.

However, as a consumer requesting the credit report directly from BNM, a consumer will only be able to obtain the Summary Credit Report, as a reference to the total exposure and conduct of the account.

How does bank define loan repayment due which appears in CCRIS report?

Certain banks classify it to be due after 1 day of the due date, but some classify it only after 14 days, or any other days. It will surely get classified if overdue for more than 30 days

How do I know if I’m blacklisted in Malaysia? If my credit application is denied by a financial institutions, does it mean that I am blacklisted?

No. Bank Negara Malaysia does not blacklist anyone as it does not express any opinion about the information in the credit report. Information on rejected credit applications is not provided in credit reports in order to ensure that a financial institution will not be prejudiced by the decision of another financial institution.

In processing loan applications, the financial institution will perform a credit assessment on the borrower. This may involve background checks from various sources. The information provided by the credit reference agencies will assist financial institutions in their evaluation. Financial institutions need to use all available data to help them make good decisions and be prudent in their loans and credits given to borrowers.

Improving your credit record in CCRIS system requires you to resolve this matter with your bank, and not from CCRIS (which is under Bank Negara)

Oh no, I miss my monthly credit card/loan repayment this month, will I be blacklisted in CCRIS immediately?

Nope, most banks will actually send you an overdue notice via email or SMS within a week after your overdue monthly repayment date. It is hard to miss this unless you ignore this ‘final reminder’. This is your last chance to pay for the month even if you genuinely forget.

If for whatever reason, you still do not pay any minimum amount, then you will be flagged in the CCRIS system for the overdue repayment.

Can I request a copy of my CCRIS report from the bank which I am applying loans and credits?

Normally, bankers or mortgage officers NOT allowed to obtain the report to give it to customers, because firstly, the Bank have to pay for such reports and therefore it is Bank’s property (for you, there are no fees to get the report). Secondly, the passing of such reports to customers is not part of the Bank’s job or approved services. Usually, the banker can inform verbally if there is a problem with the payments record in the CCRIS, but usually, he/she would advise that you personally obtain your own report if you want to know the details.

Can the information in CCRIS can be viewed/abused by other party?

The CCRIS report information can only be accessed by authorised persons in the bank and is not available to the public in general. Your credit report:

- Can only be obtained by the bank IF a formal CREDIT application is made by you to that particular bank

- Cannot be viewed by other banks, at any time

- Does not show your deposit / investment accounts

- Does not show the tenure of the credit facility enjoyed by you

- Does not show the conduct of facilities for periods above one year

I have no CCRIS record because I do not have any credit with any financial institutions. That is a good thing right?

Not at all. A Bank appreciates a GOOD CREDIT RECORD rather than ZERO CREDIT RECORD. They can’t assess you if you have nothing to show. They might think you have a bad credit history so that’s why no other banks are approving your loans.

It makes sense to have some borrowing which is ‘well-behaved’ by having on-time repayment, such as credit cards. The trick is to get your first credit facility such as a credit card.

I am taking ASB loan maxed out at RM 200k to invest in ASB because ASB gives good interests which is more than my interest I am paying for the loan. Wise decision?

Not quite if you are going to take a mortgage to buy real estate property.

ASB loan will show up as Personal Loan in CCRIS report. From a bank perspective, it may consider your monthly repayment commitment as such:

RM200,000 loan x 5% : RM10,000

This will affect your DSR (Debt Servicing Ratio) evaluation when you apply for big loans like mortgages.

What do banks typically look out for that give a bad impression?

- Accounts under legal status (legal action being taken) or special attention accounts

- Missed or late repayments

- Utilization of credit limits (E.g. A high utilization of Credit Card or Overdraft limits is an indicator of poor finances)

- High Debt Servicing Ratio (DSR). This is done via comparing your income supporting documents against the total outstanding credit

- Multiple active loan or credit applications. The more you applications you made, the more “desperate” you seem to banks. Sometimes credit approvers reject you application if they see that you have applied (and pending approve) several credit cards from several/many banks at the same time / or within a short period of time. The concern is that if the other application for credit cards get approved by the other banks at the same time, your exposure to unsecured credit goes up. So the bank processing the card now rejects your application. For example, you submitted credit card application for limit of RM 20,000 (if your salary is RM 6,500 per month) to 5 banks. In the CCRIS report obtained by the bank, it will show 5 application for credit submitted and pending approval, amounting to a total RM 100,000 unsecured credit limit. If all your application gets approved, this will make you a high risk applicant.

Any tips in improving my CCRIS record to better my chances of successfully applying for a loan?

(from LoanStreet: Everything you should know about CCRIS)

- If you have high credit utilization, pay down some your credit lines before submitting a loan application.

- A consistent string of 1’s in your repayment behaviour could indicate payment due dates that are earlier than your pay day. Try to get your bank to delay the billing cycle.

- If you have known late payment records, wait 12 months (or at least 6 months) from your last known late payment record before submitting a loan application

- Limit your amount of unsecured loan and credit applications. If shopping around, shop around first, then selectively apply for the best products. Contrary to popular practice, too many loan/credit applications actually hurt your chances of getting the best deals.

Then, watch this

I really don’t think CCRIS report is good for the public.

Without CCRIS, we will go backwards 10 years in personal financing development. Back to the days where the only place you can obtain a personal loan is to have 1 or 2 guarantors, and security deposit requirements. Furthermore, you will have no chance to apply for a personal loan except at your own existing bank which has already your track record. Back in the days (80’s) where banks insist on “introducers” i.e. you cannot even open a savings account at certain banks unless your are introduced by an existing customer of the bank.

CCRIS check and reporting provides valuable information to Banks on your money management habit when deciding to grant unsecured financing, such as a personal loan or credit cards. With a CCRIS report, approvals for financing without guarantor, collateral and salary deduction requirements are possible. Banks are willing to take more risks only if they are able to understand the consumer’s behaviour backed up by reliable data. CCRIS check and reporting fits that role.

How to banks approve credit facility?

Generally, a bank will classify the applications received as Green, Red or Amber. Ultimately, green and red is no brainer. However, for amber cases, the bank will try to improve the approval ratio by going the extra mile to salvage it.

Normally from the total applications received per month, the bank may get about 25% to 35% green cases (outright approval), 40% red cases (outright rejection) and the balance is usually Amber (KIV).

If during the month, the approval ratio is only 25%, the credit or sales team will re-look at the Amber cases to try to salvage it to increase the approval ratio to maybe 40%. Banks are profit-making organizations with high acquisition costs. Thus, if its approval ratio is less than 20%, that means it spends money to market to 100 prospects but only getting business from 20 people; which is no good business sense. The ideal target approval ratio is 40% to 55%, which indicates a good efficiency KPI.

Why my loan application rejected even though I earn high income and never had late payment history?

You have other more serious issues in your CCRIS / CTOS record that extends beyond the usual late outstanding repayment. Consult us for customized advice by clicking on the button below.

Unable to Understand Bank Rejection?

GET ONE OFF ADVICE

Why my credit card/personal loan/mortgage/car loan got rejected even though I have good credit (CTOS) score?

This may seem like a mystery to you – you want to know how the possible reasons and how to solve it?

Then click on the mini guide below to learn more.

[PTPTN Special Section]

How does overdue outstanding PTPTN loan affect you?

The latest step taken by PTPTN is to list the borrowers in CCRIS. This will affect future purchase of a house or any personal loan/car loan you apply for from banks. When the banks check on the CCRIS and saw many months of bad repayment they will reject the loan.

This section will clear your questions on how PTPTN outstanding amount affects your CCRIS

Who will be listed under CCRIS for PTPTN loan?

All borrowers who are supposed to repay PTPTN 6 months after graduation will have their name listed in CCRIS

Can I check CCRIS repayment records for PTPTN online with PTPTN itself?

No, you cannot.

What does a PTPTN potential borrower need to do to ensure he/she does not encounter issue applying for loans from banks?

PTPTN borrowers need to follow strictly the repayment schedule furnished by PTPTN. The main thing is to avoid late repayments. It is not about settling the outstanding balance.

Can a PTPTN borrower discuss his/her PTPTN repayment record with Bank Negara (BNM) or banks to get loan application approved?

No, you cannot. All discussion on PTPTN loan, whether it is about settling the outstanding balance or restructuring the repayment schedule must be done with PTPTN. Contact PTPTN branches here.

What does a PTPTN borrower need to do to ‘remove’ his or her PTPTN record from CCRIS?

A PTPTN borrower needs to settle the outstanding sum to remove his or her name from CCRIS. CCRIS record will be updated to status = SETTLED within 7 days of settling the loan.

What if a PTPTN borrower cannot afford to settle the full PTPTN loan amount but wants to avoid CCRIS related issues?

A PTPTN borrower needs to follow the repayment schedule to ensure the repayment is never late. If he or she encounter financial problems to repay, approach PTPTN to restructure the repayment schedule.

How does a PTPTN borrower request a restructuring of repayment schedule?

He or she needs to possess good conduct by not being late in repayments for the past 6 months continuously without any outstanding amount in each repayment.

If a PTPTN borrowers settled in full the outstanding loan, does his or her existing CCRIS record turn from bad to good? Can he or she now gets approved for loan application from banks?

If a PTPTN borrower has ‘bad’ repayment records in CCRIS for PTPTN loan, this record will still persist for the past 12 months before it gets ‘cleared’ because CCRIS report shows all your repayment histories for the most recent 12 months. Approval on any loan applications from banks is at the banks’ discretion.

When does a PTPTN borrower need to make monthly repayment to prevent CCRIS related issues?

To ensure monthly repayment is being updated in PTPTN system in the same month, a PTPTN borrower must make a repayment by the 27th of each month. Any repayment made after this date will only be reflected in the following month, making that repayment seen as ‘late’ by the system. This is true for all repayment channels, in general. However, any repayment made via PTPTN counters will always be updated as ‘paid’ in the same month.

Why my PTPTN repayment history is ‘bad’ in CCRIS report even though I make payment every month?

- Repayment are being made later than the schedule repayments. For example, you only start repayments to PTPTN 1 year after graduation, instead of 6 months.

- The monthly repayment is less than the scheduled monthly repayment as dictated by PTPTN. For example you only pay RM 500 whereas you should be paying RM 800.

What type of loans are easier to get approved?

Secured/collateralized loan such as a mortgage. Unsecured loans such as credit card and personal loans are categorised as very high-risk products (which also give high returns). As such, the credit criteria is the most complicated, sophisticated and most strict among the Bank’s products.

Ponder over this:

“If the customer doesn’t have enough money to pay his credit cards, housing loan and car loans, he will have to make a decision. Firstly, he will do everything to pay his housing loan, because his family needs a roof over their head. Then he will pay his car loan so that he can go to work or to the supermarket to buy groceries. Then he will pay his food bills. Credit cards always come last.”

More information at the Credit Bureau link

Good credit score makes you more attractive to opposite sex

You don’t need a fancy sports car or a killer body to impress a date.

A national study performed by Discover and Match Media Group of 2,000 American adults found that a good credit score may help land you a relationship. Match owns dating websites and apps -such as Tinder, Match.com, and OkCupid – covering 63 million global users. In Malaysia, it’s commonly known as your CTOS score.

For 58% of online daters, a good credit score is more attractive than a nice car. Half of those surveyed prefer a partner to have a good credit score over an impressive job title, and 40% took the credit score over a physically fit body.

Additionally, 69% said that financial responsibility is a very or extremely important quality when looking for a person to date. This topped the numbers for traditional traits daters look out for like a sense of humour and attractiveness, which 67% and 51% of those surveyed found important, respectively.

Financial responsibility is more important for women looking for a partner than for men. Women rated this quality as important 77% of the time, compared to 61% for men.

When asked about the personality traits of someone with a good credit score, 73% of survey respondents envisioned a responsible person, 40% thought trustworthy, and 38% equated credit scores with intelligence.

“Money talks, but your credit score can speak more about who you are as a person, and singles agree that those with good credit tend to be conscientious and reliable,” says Dr. Helen Fisher, chief scientific advisor for Match.com.

You may wonder:

How can I improve my Ccris score?

How long does being blacklisted last?

Fixing a poor credit score is easier than it sounds – and it doesn’t have to take long to boost your number.

Making on-time payments is the first step to improving your score. Scheduling automatic payments or setting up a calendar alert a few days before the due date can help make sure you never miss a payment.

It is also crucial to pay more than the minimum balance on your credit card each month. A prudent debt management approach is to focus on debts with the highest interest rate first, since paying it down will save you the most on interest charges.

Understanding someone’s financial security early in a relationship can help avoid further issues.

A majority – 53% – of respondents said finances had strained a past or current relationship. This makes money a bigger wedge in relationships than politics or religion, two topics that are practically taboos for a first date.

source: Business Insider

Now It’s Your Turn

Phew! We put A TON of work into this check CCRIS online guide. So we hope you find it useful.

Now we’d like to hear what you have to say.

What’re the CCRIS matters that we didn’t cover in this guide?

Let us know by leaving a comment below.

When will the status of Application of Credit be remove from the list as it is rejected when i check with the bank?

from ‘the list’? What list are you referring to?

Hi, I used to have legal status,NPL owing to two banks like 5 years back. I recently generate from CTOS and RAM, and the report doesn’t show any of it now it’s like a clean report. Does it mean I am clear to proceed applying for Credit Card and Loans? Also what is the meaning of CCRIS entity key?

If your credit report does not show any legal status, you are ‘clear’ ! 🙂

Where are you seeing this CCRIS entity key?

Hi, I am wondering how do i get the banks that i owe to update the ccris report as per current outstanding (that I calculated myself). It’s been 2 years and some of the banks still no latest update. I called them recently to find out the possible full settlement amount and its not far off from my calculation. But it’s depressing that the outstanding balance is not current. This should not happen, correct?

Another thing, i do have outstanding of RM3k that is blaring red in my PTPTN statement, is that what’s appearing as arrears in CCRIS report? I was in red for almost 2 years, hence there are arrears in payment. But now m paying it back on time. I know it’s gonna take sometime to clear up, but wondering what’s appearing as arrears on CCRIS-PTPTN for 22 months.

Means you are late for 22 months on your PTPTN payment – this has nothing to do with your total outstanding.

I have legal status in my ccris, how long it will appear, even though I have settle that fees, and can give suggestions how to solve, should I sell that house(housing loan) tq in advance

have u asked banks directly?

my current CCRIS report shows Judgement order / Order of sale due to car loan. On july i already made full settlement and already got release latter from bank. FYI my CCRIS arrears shows 0 for 12 months. my question is how long will the judgement order be cleared from record?

Are you referring to CCRIS report gotten from e-CCRIS BNM website or the CTOS report bought from CTOS?

Hi sir, may I have your opinion as previously I missed my personnel loan payment for months due to missed communication with banker. So my criss report showing 2 for the first 6 months. If I make full settlement now, will the record in criss cleared or the bad payment record still show there until 12months later?

12 months later no more dude 🙂

Dear Sir,

I have CCRIS issue due to PTPTN loan arrears. I have outstanding balance of RM7000. If I clear the full outstanding amount. Will it clear my CCRIS issue and I have planned to invest some amount as FD as well. And planning to set PTPTN payment as auto debit payment as well for every month.

Will this help me in improvising my CTOS score and settle the CCRIS issue?

Thanks and regards,

Muhamad

yes it will but takes time

Hi,

I have few npl with 3 banks. But i recently checked my ccris report n ctos, non of these npl records appears. How this could happen ? M i free to apply loans with bank since my ccris report is clear ?

wow, you can be the lucky few! 🙂

Hi sir,in my situation.i have made a loan for car with different bank (7 banks) but.got rejected because got a lot of scoring system issue rejected list and not because of my salary.it is my name in scoring system permanently or will delete.? And when i need to apply the new loan again? Thanks .

first is to find out WHAT is wrong with your credit rating. It’s like if you have a gun, but you don’t know where is the target, it won’t help much